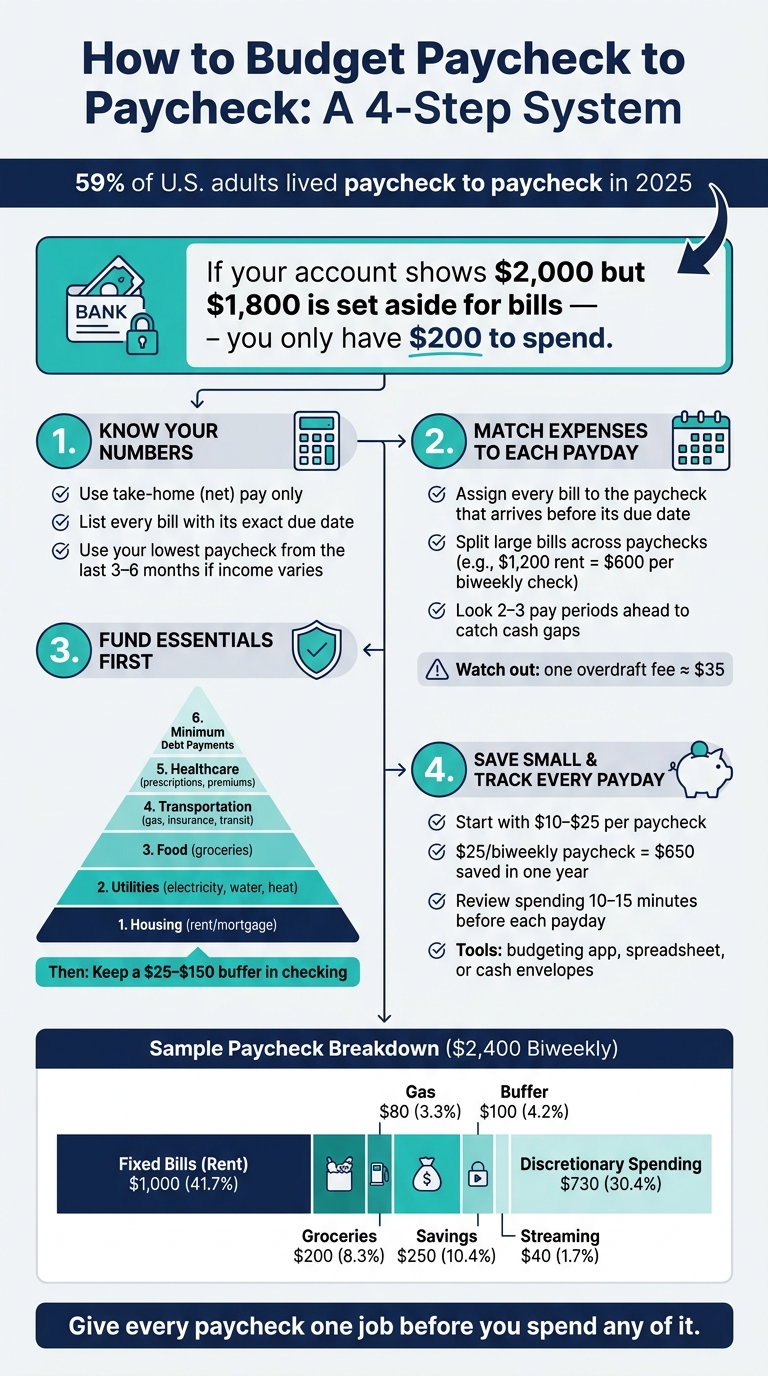

If I live paycheck to paycheck, I need a plan for timing, not just totals. In 2025, 59% of U.S. adults were in the same spot. The fix is simple: I match each paycheck to my bills, cover basics first, keep a small buffer in checking, and save even $10 to $25 per paycheck when I can.

Here’s the whole idea in plain English:

- I budget with take-home pay, not gross pay.

- I list every bill with its due date.

- I assign each bill to the paycheck that comes before it.

- I split big bills across checks when one paycheck can’t cover them alone.

- I fund housing, utilities, food, transportation, health costs, and minimum debt payments first.

- I put a small $25 to $150 cushion in checking to help avoid overdrafts.

- I track each pay period and adjust before the next one.

If my account shows $2,000, but $1,800 is already set aside for rent and other bills, I do not have $2,000 to spend. I have $200.

That’s the core rule.

I also need to watch for cash gaps. A late bill or overdraft is often a timing problem. And with overdraft fees often around $35, bad timing gets expensive fast.

Bottom line: I do better when I give every paycheck one job before I spend any of it.

To keep it simple, I focus on these four steps:

- Know my paychecks, bills, and due dates

- Match expenses to each payday

- Cap flexible spending

- Build a small savings cushion and review often

This article lays out that system in a way I can use every payday.

Paycheck-to-Paycheck Budget System: 4 Steps to Take Control

1. Start with take-home pay, fixed bills, and due dates

Calculate net income by paycheck

Once you know your payday schedule, build your budget around the money that actually hits your bank account. Use net pay - the amount deposited after taxes and deductions. Skip gross pay and any “on paper” hours that may not turn into cash.

Also, keep overtime, bonuses, commissions, and tax refunds out of your main budget. They’re not steady. If that money comes in, great - send it to savings or debt payoff. But your base plan should depend only on income you can count on every single pay period.

If your pay goes up and down, use the lowest regular paycheck from the last three to six months as your starting point. It gives you a steadier plan, even during slower weeks.

Separate fixed costs from variable spending

Now split your spending into two buckets: what must be paid and what can move a bit.

Fixed expenses are bills that usually stay about the same each month, like rent, a car payment, car insurance, internet, and subscriptions. They come with set due dates and amounts that don’t change much.

Variable expenses are things like groceries, gas, and household supplies. You need them, but the total can shift from week to week.

To get numbers you can trust, check your bank and credit card statements from the last 30 to 60 days. Go line by line. Watch for charges that are easy to miss, like annual subscriptions or quarterly fees. When you write each bill down, round it up to the nearest dollar. That small buffer can help more than you’d think.

List due dates before assigning money

After you know the amounts, put every bill on a calendar. Make one master list of recurring bills with the exact due date for each one. For example: rent on the 1st, car insurance on the 5th, internet on the 10th, utilities on the 15th, car payment on the 20th, and cell phone on the 25th. That list should guide each payday decision.

Here’s why this matters: if most of your bills hit in the first week of the month but your paycheck lands on the 5th, that’s a cash-flow problem, not an income problem. In that case, ask service providers if they can move your due dates so they line up better with your paydays.

sbb-itb-02fd20a

2. Map every expense to each payday

Give every expense a job before you spend a dollar. The idea is simple: match each bill to the paycheck that will pay it. That way, every payday has a clear purpose instead of turning into a guessing game.

Think of each paycheck as its own mini bill cycle.

Match bills to the paycheck before the due date

Go through every bill on your master list and tie it to the paycheck that comes in before the due date. Then set that money aside right away.

If rent is due on the 1st and you get paid on the 15th and 30th, the paycheck on the 30th covers rent. That money is already spoken for.

Some bills are too big to come out of one check without squeezing everything else. In that case, split the cost across paychecks. If your rent is $1,200 and you're paid biweekly, set aside $600 from each paycheck. You can use the same approach for car payments and other large fixed bills.

Spot cash gaps and overdraft risk early

This step helps you catch trouble before it hits your bank account.

A cash gap happens when several bills are due in a short stretch before the next paycheck arrives. Look ahead two to three pay periods at a time so you can see those tight spots early. If rent, a car payment, and a utility bill all hit within a few days, that's a warning sign.

A single overdraft fee is typically around $35. That adds up fast, especially when the issue is timing, not total income.

If a bill keeps landing in the wrong week, reach out to the provider and ask to move the due date so it lines up better with your pay schedule.

A sample paycheck budget breakdown

Here’s a sample biweekly paycheck breakdown for a $2,400 paycheck:

| Category | Amount |

|---|---|

| Fixed Bills | Rent ($1,000) |

| Variable | Groceries ($200), Gas ($80) |

| Savings | $250 |

| Buffer | $100 |

| Discretionary | Streaming ($40), Spending Money ($730) |

Your spendable cash is whatever is left after bills, savings, and buffer amounts have been assigned.

For example, if $2,000 is sitting in your account but $1,800 is already set aside for upcoming rent and bills, your spendable cash is $200. To make that number easier to use day to day, divide it by the number of days until your next paycheck. That gives you a daily spending cap.

With each paycheck assigned, the next step is to cover essentials first and limit flexible spending.

3. Fund essentials first and cap flexible spending

Once each expense is mapped, fund the basics first: housing, utilities, groceries, transportation, healthcare, and minimum debt payments. After that, put firm limits on flexible spending so each paycheck has a job and doesn't drift off course.

Cover the core categories before extras

Start with the bills and costs you can't dodge. That means rent or mortgage first, then utilities, food, transportation, healthcare, and minimum debt payments.

| Priority | Category |

|---|---|

| 1 | Housing (rent, mortgage) |

| 2 | Utilities (electricity, water, heat) |

| 3 | Food (groceries) |

| 4 | Transportation (gas, car insurance, transit pass) |

| 5 | Healthcare (prescriptions, insurance premiums) |

| 6 | Minimum Debt Payments (credit card minimums, car payments, student loans) |

If money is tight, switch to a bare-bones budget and fund only these categories before any optional spending, like dining out, streaming, or entertainment.

Set realistic limits for groceries, gas, and personal spending

Look back at the last two to three months of bank statements and find your actual average for groceries and gas. Then use the high end of that range to give yourself a little room. For example, if grocery spending usually lands between $90 and $110 per week, budget $110.

Some categories are easier to overspend in than others. Groceries, gas, and personal spending can slip fast. In those cases, a weekly cap often works better than a monthly one. It's simpler to spot a problem after one expensive week than at the end of the month when the money is already gone.

Keep a small buffer in your checking account

After you've funded the basics and set your flexible limits, keep a small buffer in checking - usually $25 to $150. This isn't extra spending money. Think of it as a shock absorber.

It can help cover:

- a bill that comes in a little higher than expected

- a charge you forgot about

- a timing gap between payday and when a bill clears

With essentials covered and a buffer in place, the next move is building a small savings cushion and tracking every paycheck.

4. Build a small savings cushion and track your plan

Start with small savings targets that work in tight months

When money is tight, start small. $10 to $25 per paycheck is enough to get moving. It may not feel like much at first, but it adds up. Save $25 from each biweekly paycheck, and you’ll have $650 over a year.

That small cushion can cover timing gaps and help you avoid overdrafts. After that, aim for $500, then build toward one month of basic expenses.

Set up the transfer for the day after payday so the money moves before you’re tempted to spend it. Then handle each paycheck the same way.

Pick one tracking method and use it every payday

Tracking helps each paycheck match your bills, savings, and day-to-day spending. The big thing here is consistency. If you bounce between tools in the middle of the month, it gets messy fast.

Here are three simple options that work well for paycheck budgeting:

- A budgeting app like Monefy helps you log groceries, gas, and daily purchases as they happen. Real-time balances make overspending hard to miss.

- A basic spreadsheet in Google Sheets works well if you want more control. It’s free, flexible, and does require you to log things by hand.

- Cash envelopes can help with categories where you tend to overspend, like dining out or personal spending. When the envelope is empty, you stop spending.

Track groceries, gas, and small daily purchases before the money disappears.

Review and adjust before the next pay period

Before each payday, take a quick look at what changed. Spend 10 to 15 minutes reviewing the previous pay period. Check where you went over, update bill amounts, and adjust the next paycheck before you assign the money.

Also check upcoming bills and your checking account buffer. If your income shifts or a major expense pops up, update the budget right away. That short review can help you spot problems before the next payday and carry those fixes into the next paycheck.

Conclusion: Use each paycheck with a plan, not guesswork

As Shelter puts it, "Living paycheck to paycheck is often a cash flow timing problem, not purely an income problem." That idea gets to the heart of it. The point isn’t to sit around waiting for a bigger paycheck. It’s to use each one on purpose.

Budgeting by payday helps turn money from a monthly guessing game into a repeatable plan. Start with your take-home pay. Match it to your bill due dates. Cover essentials first, then keep a small buffer so one off week doesn’t throw everything off.

Put simply: give every paycheck a clear job. You don’t need perfect income to do that. You need a system you can repeat every payday. And when those small habits show up again and again, you start to get real control over your money.

FAQs

What if my paycheck amount changes each pay period?

If your paycheck goes up and down because of tips, hourly shifts, or gig work, build your budget around your lowest recent paycheck instead of using an average or a strong month.

That gives you a safer starting point for covering your main bills. Then, if one pay period comes in higher than expected, you can put the extra money toward savings, debt payoff, or other goals.

How do I handle bills due before payday?

Write down your recurring bills and their due dates. Then contact each provider and ask if they can shift your billing date so it lines up better with your paycheck.

When your paycheck hits, set aside money right away for any bills due before your next payday. Treat that money as off-limits, not extra cash sitting in your account.

If your rent is due on the 3rd but you get paid on the 15th and 30th, you can probably see the problem. Moving due dates can take some pressure off and make your cash flow feel less chaotic.

It also helps to build a small cash buffer over time. Aim for $300 to $800 so you can cover short gaps without scrambling.

How much buffer should I keep in checking?

A checking account buffer, sometimes called a float, gives you a little breathing room for small timing gaps and surprise costs. The idea is simple: it helps you avoid overdrafts without dipping into your emergency fund.

A good starting point is $50 to $150 for minor day-to-day swings. If you want a bigger cushion, keep $500 to $1,000 in the account.