Most family budgets fail for one simple reason: they don’t match the money that hits the bank or the dates bills are due. If I want a budget to work, I need to build it from net income, use recent spending, set limits for fixed and variable costs, and leave space for savings, debt, and surprise bills.

Here’s the short version:

- I start with take-home pay, not gross income.

- I review the last 2–3 months of bank and card statements.

- I split spending into fixed bills, variable costs, and optional spending.

- I set caps for groceries, gas, childcare, and debt based on what I already spend.

- I add a 2%–7% buffer for random costs.

- I check the budget weekly and reset it monthly.

- If income changes, I rebuild the plan right away.

A family budget works best when it is simple, honest, and used every month. The goal is not a perfect spreadsheet. The goal is a plan that helps me cover bills from the start of the month to the end without running short.

A few numbers from the article stand out:

- Childcare can run $1,500–$2,000 per month per child

- Many families land closer to 60/20/20 than 50/30/20

- A starter emergency fund of $1,000 is a common first target

- More than 50% of Americans say they could not cover an unexpected bill over $2,500

If I had to boil the whole article down to one idea, it would be this: a budget has to match actual life, not wishful thinking.

Get Clear on Your Family's Income and Spending

Before you set limits, start with two numbers that come from real life, not guesses: net income and actual spending from your recent statements.

Bring Both Partners Into the Process

Set up a short money meeting. 15 to 30 minutes is enough. The goal is simple: get both partners looking at the same numbers before you decide on any category limits.

Keep the meeting focused on facts, not fault. This isn't about picking apart past spending. It's about getting on the same page. Choose two or three shared priorities, like paying down debt, building an emergency fund, or saving for a known expense that's coming up. Write them down.

Those priorities become the reason behind your budget. When a spending choice comes up later, you won't be deciding in a vacuum. You'll be measuring it against what matters most to your household.

List Income the Way It Actually Arrives

Always build your budget around net income - the money that actually hits your bank account after taxes, health insurance premiums, and retirement contributions are taken out. If it doesn't land in the account, don't budget it.

Your monthly starting point depends on how you're paid:

| Pay Type | How to Calculate Monthly Income |

|---|---|

| Salaried | Add up all take-home deposits received within a 30-day period |

| Weekly or biweekly | Total the actual take-home checks that landed in the month |

| Freelance or gig | Average the last 3 to 12 months of net earnings |

| Commission or seasonal | Use the lowest realistic month from the past year as your floor |

If you or your partner does freelance or contract work, move 20% to 30% of that income aside for taxes right away - and don't treat it as part of the household budget. If extra income comes in, give it a job on the spot: debt, savings, or an upcoming bill. Otherwise, it tends to vanish into day-to-day spending.

Sort Spending Into Fixed, Variable, and Optional Categories

Pull the last two to three months of bank and credit card statements and review every transaction. Then sort each one into three buckets:

- Fixed essentials - costs that stay the same each month and aren't up for debate, like rent or mortgage, car payment, insurance premiums, childcare, internet, and minimum debt payments

- Variable essentials - costs you need but that change month to month, like groceries, gas, utilities, prescriptions, and household supplies

- Optional spending - everything else, including dining out, streaming subscriptions, hobbies, and entertainment

Auto-categorized transactions can help you get started, but don't stop there. Clean them up. The point of this step is to catch the spending that's easy to miss: old subscriptions, impulse purchases, and recurring fees that quietly drain cash.

Once every transaction has a place, you can set monthly limits based on what your family is actually doing - not what you hope the numbers look like.

Once income and spending are mapped, the next step is setting category limits that fit real numbers.

sbb-itb-02fd20a

Set Monthly Spending Limits Based on Real Numbers

Family Budget Spending Limits by Family Size (2024)

Now turn those category totals into monthly limits. The goal is simple: set spending caps that match your actual cash flow, not an ideal version of it.

Cover Essentials Before Wants and Financial Goals

Start with the bills you must pay first. That means housing, utilities, groceries, transportation, insurance, minimum debt payments, and required childcare.

After that, make room for:

- a small emergency fund

- sinking funds

- extra debt payoff

- discretionary spending

That order matters. If you do it backward, the budget can look fine on paper and still fall apart by the middle of the month.

Compare your total essential spending with your monthly net take-home pay. If essentials already use 55% to 60% of take-home pay, don’t just trim a few lines and hope for the best. Redesign the budget.

Use the 50/30/20 Rule as a Starting Point

The 50/30/20 rule - 50% for essentials, 30% for wants, and 20% for savings and debt - is a good place to begin. But it’s a tool, not a rule carved in stone.

A lot of U.S. families, especially those with young kids or living in high-cost cities, just won’t fit neatly into that split.

If daycare runs $1,500 to $2,000 per month per child, and in many places that rivals or even beats a mortgage payment, your essentials share will climb on its own. That’s not a budgeting failure. That’s math.

Use 50/30/20 as a baseline, then adjust for childcare and housing. Many families land closer to a 60/20/20 split.

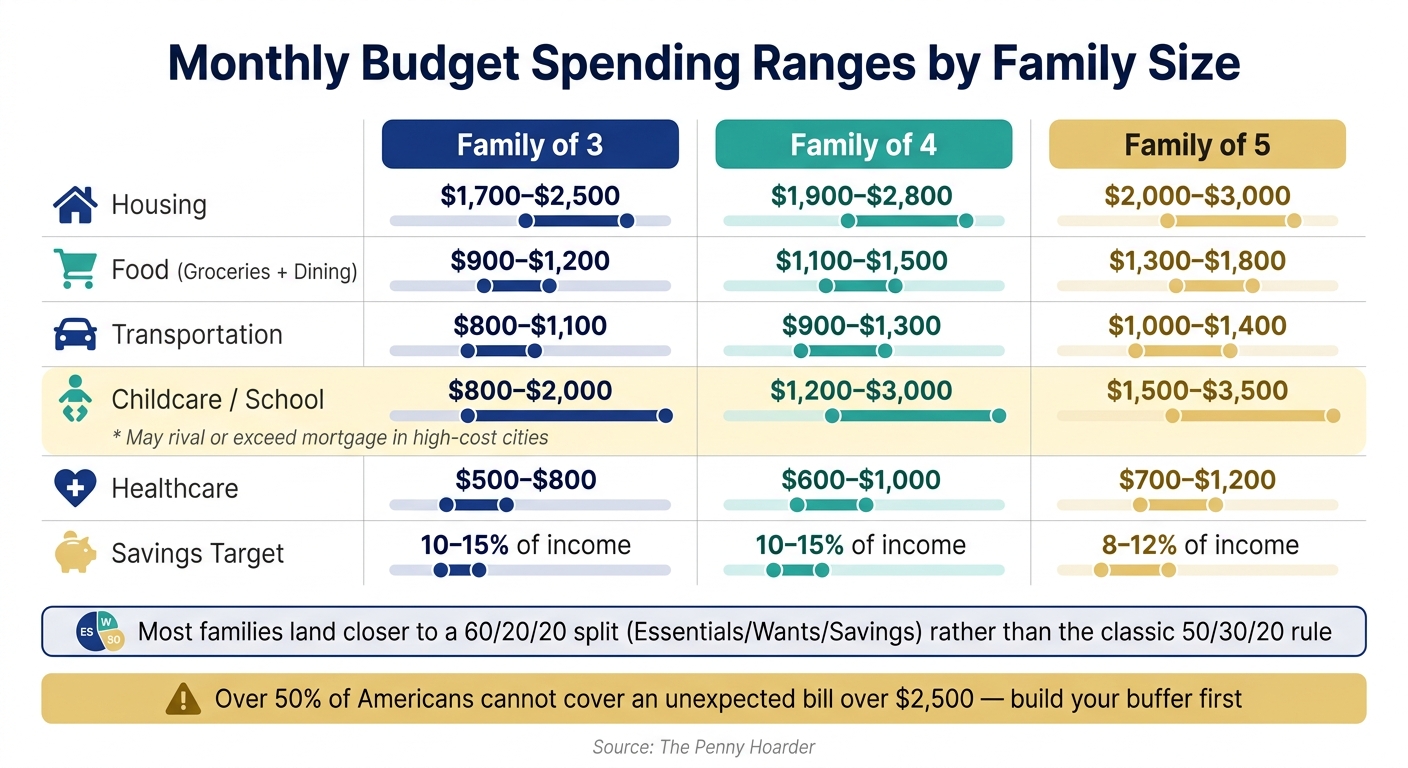

Set Limits for Groceries, Childcare, Transportation, Debt, and Sinking Funds

Once you know your averages, turn them into caps. These ranges can help you sanity-check your plan:

| Category | Family of 3 | Family of 4 | Family of 5 |

|---|---|---|---|

| Housing | $1,700–$2,500 | $1,900–$2,800 | $2,000–$3,000 |

| Food (Groceries + Dining) | $900–$1,200 | $1,100–$1,500 | $1,300–$1,800 |

| Transportation | $800–$1,100 | $900–$1,300 | $1,000–$1,400 |

| Childcare / School | $800–$2,000 | $1,200–$3,000 | $1,500–$3,500 |

| Healthcare | $500–$800 | $600–$1,000 | $700–$1,200 |

| Savings Target | 10–15% of income | 10–15% of income | 8–12% of income |

(Source: The Penny Hoarder)

Sinking funds are for bills you know are coming, just not every month. Think car registration, holiday gifts, back-to-school shopping, or annual insurance premiums.

Take each yearly total, divide it by 12, and move that amount every payday. Automating those transfers on payday makes life a lot easier. Then check your limits each week so small overruns don’t turn into a bigger mess.

Track Your Budget and Adjust It When Life Changes

Once your category limits are set, the next step is simple: track what happens. A budget doesn’t work on good intentions alone. You have to check spending, spot overruns, and change the plan when life changes.

Choose a Tracking System Your Family Will Use

You don’t need the perfect system. You need one your family will stick with.

| System | Best For | Setup Tip |

|---|---|---|

| Budgeting App (Monefy) | Busy families needing automation | Enable multi-device syncing and push notifications for reminders |

| Spreadsheet | Partners who want a deep-dive review | Use a "Planned vs. Actual" template and review it together monthly |

| Cash Envelopes | Controlling impulse spending | Withdraw a set amount of cash for groceries or dining at the start of the month |

With Monefy, you can create custom categories for kid-related costs and let both partners log expenses from their own devices. That makes day-to-day tracking a lot easier, especially when spending comes from more than one person.

Add a Buffer for Surprises and Start Building Emergency Savings

Even a well-planned budget gets hit with random costs. School field trips. Medical copays. That one extra fee you forgot was coming.

Build in a 2% to 7% miscellaneous buffer for small surprises. Then start an emergency fund with $1,000 and automate transfers after each payday. After that, aim for $2,500 for bigger shocks, and then build toward three to six months of essential expenses for long-term stability.

The numbers here are hard to ignore. Only 37% of working Americans maintain a dedicated emergency fund, and more than 50% say they couldn’t cover an unexpected expense over $2,500. That’s the difference between a budget that bends and one that breaks.

Check In Weekly, Reset Monthly, and Revise After Big Changes

A short weekly check-in can save you from a mess later. Set aside 10–15 minutes every Sunday to review what you spent that week and flag anything going over. Keep it factual, not emotional. This small habit helps you catch leaks like unused subscriptions or impulse buys before they spill into the next category.

Then do a monthly reset together. Spend 15–30 minutes at the end of each month comparing what you planned to spend with what you actually spent. If one category keeps running high, decide whether you need to cut back or move money from somewhere else.

The first 90 days usually take some trial and error. Grocery costs, kids’ activities, and other variable expenses are often off in the beginning, and that’s normal.

When your numbers change, update the budget right away instead of waiting for the next month. A job change, a new baby, a move, or a major medical bill can throw off the whole plan. Recalculate your income, reset your fixed costs, and rebuild your category limits from the ground up. Then update those numbers in Monefy or your spreadsheet so your budget matches your actual life.

Fix the Most Common Family Budgeting Problems

Use these fixes when your budget starts slipping.

Overspending, Impulse Buys, and Subscription Creep

If one budget category keeps going over, don't guess. Reset it using three months of actual spending.

Then tighten things up with a few simple habits. Split your monthly grocery limit into weekly caps. For example, $150 per week often feels easier to manage than $600 per month. Log transactions every couple of days so small purchases don't vanish from memory. And before any non-essential purchase, use a 24-hour wait rule. That pause can stop a lot of "why did I buy that?" moments. It also helps to keep a small fun-money category, so the budget still feels usable instead of restrictive.

Recurring charges can also eat away at your cash without much warning.

Look through three months of statements, cancel subscriptions you no longer use, and then reset that category.

Debt Pressure, Partner Disagreements, and Irregular Income

Debt feels less overwhelming when all the numbers are in one place. List every balance, interest rate, and minimum payment. Then pick a payoff method and stick with it.

| Method | How It Works | Best For |

|---|---|---|

| Debt Snowball | Pay off the smallest balance first, then roll that payment to the next | Building momentum with quick wins |

| Debt Avalanche | Pay off the highest interest rate first | Saving the most money over time |

Both methods work. The better choice is the one you'll keep using.

Debt also gets easier to handle when both partners are looking at the same numbers.

Use shared visibility, agreed categories, and personal spending allowances to cut down on conflict. Start with the big-picture goals so the budget feels like a team effort. Then give each partner a monthly personal spending allowance. That can ease tension around small purchases.

For irregular income, use one of these two approaches:

| Approach | Strategy | Best For |

|---|---|---|

| Conservative Baseline | Budget based on your lowest recent monthly income; treat anything extra as bonus savings | Highly variable income (commissions, seasonal work) |

| Monthly Averaging | Average the last 3–6 months of take-home pay to set your monthly budget | Freelance or consistently fluctuating income |

If you're self-employed or freelancing, set aside 20% to 30% of every payment for taxes before you count the rest as household income.

Once you fix the weak spots, keeping the budget month after month gets a lot easier.

Conclusion: A Family Budget That Works in Real Life

Start with real take-home income, set limits based on actual spending, and do a short check-in every week. When life changes, update the numbers right away.

FAQs

How do I budget if my income changes every month?

When your income goes up and down, build your budget around the lowest monthly amount you can count on. That way, your must-pay bills are covered even in a slower month.

Another option is to use your average income from the past three to six months. Just make sure you keep a buffer for months when earnings dip.

Then, when you have a better month, set the extra aside. You can use it to build a buffer or add to a sinking fund. This income smoothing approach helps you keep spending steady and your finances on track.

What should I do if our essentials already take most of our pay?

If basics eat up most of your paycheck, start by trimming the extras. That means things like dining out, streaming services you don’t use much, and other non-essential subscriptions. For your biggest bills, see if there’s another way to handle them. A flexible work schedule or help from family with childcare, for example, can take some pressure off.

Then put what’s left toward your core needs and an emergency fund. Even a small start counts. Keep optional spending on a short leash so you can hang on to your savings.

How much emergency savings should my family build first?

Start with a $1,000 emergency fund. Think of it as your first line of defense. If your car breaks down or you get hit with a medical bill, that cash can help you cover the cost without turning to a credit card or loan.

Once that starter fund is in place, aim for 3 to 6 months of household essentials. That usually means things like rent or mortgage payments, groceries, utilities, insurance, and other must-pay bills.

If your income goes up and down from month to month, or your household depends on one paycheck, it often makes sense to save 6 to 12 months instead.