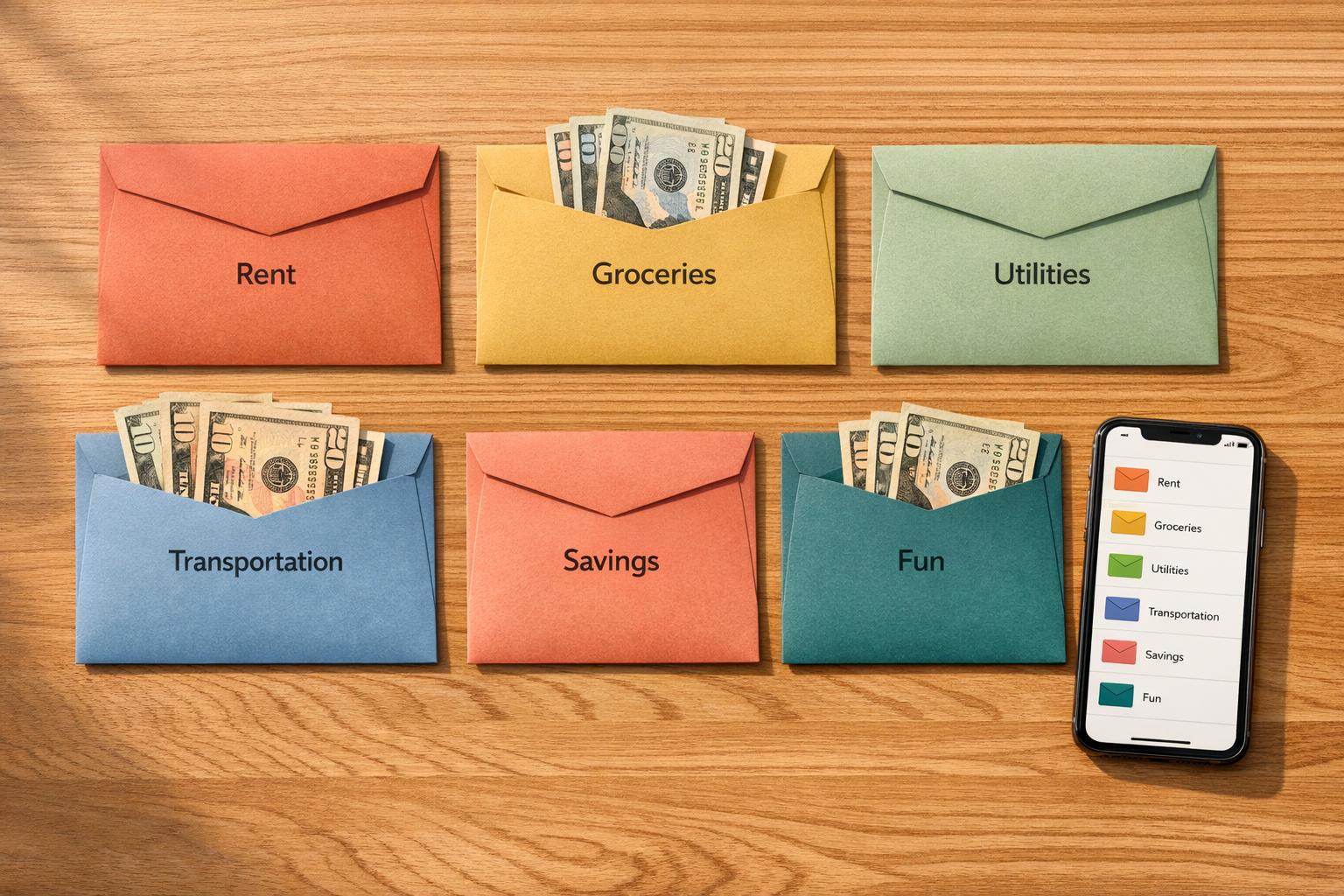

Envelope budgeting is a simple way to manage your money by dividing your income into specific spending categories. Each category gets its own "envelope" (physical or digital), and you only spend what's inside. When an envelope is empty, spending for that category stops until your next paycheck. This method helps control variable expenses like groceries or entertainment, prevents overspending, and encourages saving by setting clear boundaries.

Key Steps to Start:

- Calculate Income: Use your net income (after taxes) to set a baseline.

- Identify Categories: Focus on 3–4 key spending areas like groceries, gas, or dining out.

- Allocate Funds: Distribute money across categories based on priorities.

- Use Envelopes: Choose physical cash or digital tools to track spending.

- Monitor Weekly: Adjust as needed and decide how to handle leftover funds.

Studies show cash-based systems can reduce spending by 12–18%, making this approach effective for controlling habits. Apps like Monefy offer a digital twist, combining ease of use with the discipline of envelope budgeting.

How Envelope Budgeting Works

5 Steps to Start Envelope Budgeting

Envelope budgeting transforms your income into a clear, manageable spending plan in just five steps. Each step builds on the previous one, making it easier to track and control where your money goes.

Step 1: Calculate Your Income

Start with your net income - the money you actually take home after taxes and deductions. Include all consistent income sources like your paycheck, regular side gig earnings, or government benefits such as Social Security. Avoid factoring in one-time bonuses or irregular income, as these can skew your budget.

For those paid biweekly, you can estimate your monthly income using this formula: (net pay × 26) ÷ 12. If your income varies, use the lowest amount you've earned in the past three to six months to create a more reliable baseline.

| Income Type | Include | Exclude |

|---|---|---|

| Primary Wages | Net take-home pay | Gross salary before deductions |

| Side Hustles | Consistent, recurring earnings | One-off gigs or unpredictable bonuses |

| Benefits | Regular aid like Social Security | Tax refunds or one-time payments |

| Variable Income | Lowest earnings in the last 3–6 months | Average or "best-case scenario" amounts |

Step 2: Identify Spending Categories

Take a close look at your checking account and credit card statements from the last three to six months. This will help you see where your money is actually going, rather than relying on guesses. Focus on variable expenses - those that fluctuate monthly - like groceries, gas, dining out, and entertainment. Fixed bills, such as rent or subscriptions, are better handled through automatic payments.

Start with just three to four key areas where you tend to overspend. Popular categories include:

- Groceries

- Gas

- Dining out

- Entertainment

- Clothing

- Personal care

You might also want to create a "Miscellaneous" or "Buffer" envelope for unexpected small expenses. For irregular costs like car repairs or holiday gifts, set up "sinking fund" envelopes by dividing the annual expense by 12. These categories will guide how you allocate your income in the next step.

Step 3: Allocate Funds to Categories

Distribute your income across your chosen spending categories based on your priorities and past habits. Using round numbers (like $200 or $300) makes tracking easier. If you're budgeting with a partner, consider setting up individual "Personal Spending" envelopes for discretionary use.

"If it works with your income, the 50/30/20 budget is one simple method for people starting to organize their finances. This budget allocates 50% of your income for essentials, like rent and bills; 30% to personal day-to-day spending; and 20% for savings or financial goals."

- Brian Walsh, CFP and Head of Advice & Planning, SoFi

Focus on covering discretionary spending - what's left after fixed bills are paid. Once you've allocated funds, you're ready to manage your spending using physical or digital envelopes.

Step 4: Use Physical or Digital Envelopes

Physical envelopes involve withdrawing cash on payday and dividing it into labeled envelopes for each category. When withdrawing, ask for smaller denominations to make allocation easier. Track spending by noting the remaining balance in each envelope.

Digital envelopes, on the other hand, use budgeting apps or separate bank sub-accounts to divide your funds. Transactions can be logged manually or synced with your bank to update balances automatically. Using a budgeting app can streamline this process by categorizing transactions in real-time. Many apps now offer tools like receipt scanning or voice input to simplify tracking.

A hybrid approach combines both methods. For example, you might use cash for categories like dining out (where overspending is common) while managing other expenses digitally. This gives you the best of both worlds - tangible control with modern convenience.

| Feature | Physical Envelopes | Digital Envelopes |

|---|---|---|

| Psychological Impact | High (cash feels more "real") | Moderate (numbers on a screen) |

| Convenience | Lower (requires ATM trips) | Higher (integrated with online tools) |

| Tracking | Manual (write balances on envelopes) | Automatic or app-assisted |

| Security | Risk of cash loss or theft | Protected by bank/app security |

| Best For | Tactile learners, overspenders | Tech-savvy users, online shoppers |

Regularly check your progress and adjust as needed to stay on track.

Step 5: Monitor and Adjust

Review your envelope balances weekly to ensure you're pacing your spending throughout the month. Try not to "borrow" from other envelopes unless it's an emergency.

At the end of the month, decide what to do with leftover funds. You can roll them over, add them to savings, or reallocate them to categories that fell short. Some people prefer filling envelopes weekly instead of monthly to avoid overspending early on.

If you find yourself consistently running short in one category, adjust your allocations next month to better reflect your needs.

"I would recommend the envelope system for ANYONE wanting to budget successfully."

- Jenny Groberg, CEO and Founder, BookSmarts Accounting and Bookkeeping

sbb-itb-02fd20a

Benefits of Envelope Budgeting

Envelope budgeting sets clear spending boundaries, making it easier to manage your finances without guesswork. Once an envelope runs out of cash, spending in that category stops. This approach prevents mixing funds, so money earmarked for essentials like rent doesn't accidentally get used for non-essentials. It reinforces disciplined spending habits throughout the month.

Another advantage is that using physical cash can curb impulsive spending. Studies show that cash-based systems reduce spending by 12–18% compared to card usage. The act of withdrawing money from a specific envelope makes you think twice before making an unplanned purchase.

This method also helps you avoid overdrafts and credit card debt because it ensures you only spend what you've set aside. Plus, savings become a priority since you fund your savings envelope first, rather than relying on leftover money at the end of the month.

The visual aspect of envelope budgeting is equally powerful. Seeing the balance in each envelope helps you pace your spending and make thoughtful trade-offs when needed.

| Benefit | How It Works | Real Impact |

|---|---|---|

| Reduced Overspending | Spending is limited to the cash in each envelope | 12–18% less spending compared to card use |

| Better Savings | Savings are treated as a priority, not an afterthought | Encourages consistent saving habits |

| No Overdrafts | Spending is capped by the amount allocated | Lowers the risk of overdraft fees and debt |

| Clear Trade-offs | Moving funds between envelopes shows opportunity costs | Promotes thoughtful financial decisions |

Who Can Benefit from Envelope Budgeting?

Envelope budgeting is particularly helpful for people who face specific financial challenges. For chronic overspenders or visual and tactile learners, this system can be a game-changer. Unlike the seamless (and often invisible) nature of card transactions, envelope budgeting uses physical cash, which makes spending feel more real. Watching the cash in an envelope dwindle provides immediate feedback that a digital notification just can’t replicate. It’s a powerful way to set boundaries and avoid blending funds meant for different priorities.

This approach is flexible enough to suit a range of financial goals. For budgeting beginners, it’s straightforward - no need for spreadsheets or complex math. It’s also a great tool for couples who want a shared system to manage their finances. Physical envelopes make it clear what funds are available, reducing the chance of miscommunication. For those focused on aggressively paying off debt, envelope budgeting is especially effective. It creates firm, non-negotiable limits that ensure every dollar is working toward debt repayment.

"The empty envelope doesn't lie, doesn't negotiate, and doesn't accept excuses" - SenticMoney

The rules are simple: when an envelope is empty, spending in that category stops - no exceptions.

To get started, focus on 3–4 major spending categories, such as dining out or entertainment. Trying to divide every expense into a category right away can feel overwhelming, so keep it simple at first. Including a "Miscellaneous" envelope can also help cover unexpected costs, making the system less rigid and easier to stick with. Regularly checking your envelope balances throughout the month ensures you stay on track and don’t run out of cash prematurely.

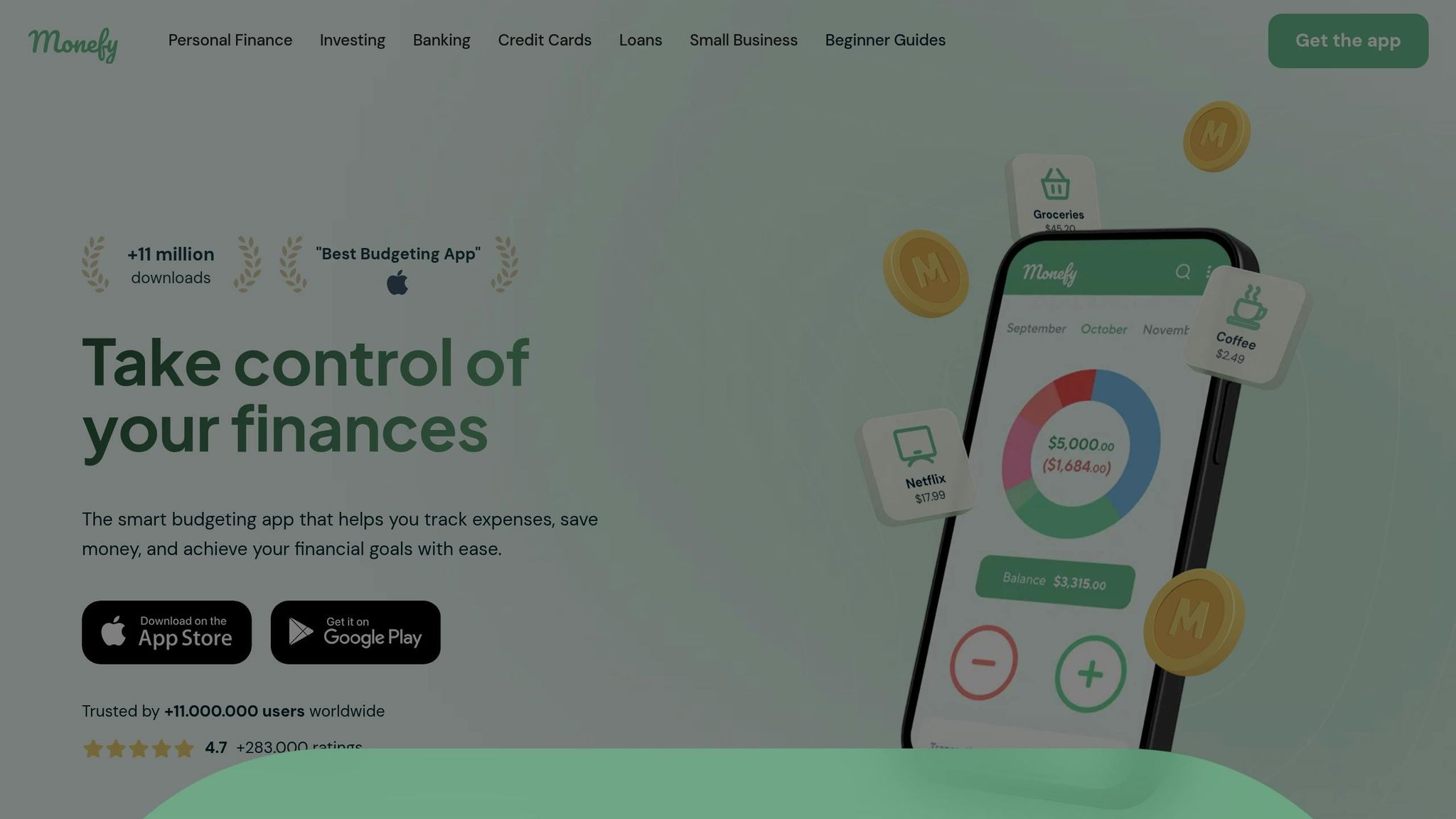

Using Monefy for Envelope Budgeting

Monefy takes the traditional concept of envelope budgeting and gives it a digital twist, making it easier to manage your expenses without relying on physical cash. With this app, you can allocate your monthly budget into customizable categories that act as virtual envelopes. Categories like "Groceries", "Dining Out", or "Entertainment" show how much you’ve spent and what’s left, giving you a clear, real-time picture of your spending.

One standout feature of Monefy is its manual entry system. Unlike apps that automatically sync with your bank account, Monefy requires you to log each transaction yourself. This extra step mirrors the experience of handling physical cash, increasing your awareness of where your money is going and helping you stay in control.

"Monefy transforms budgeting from a tedious spreadsheet task into a simple, visual experience that takes seconds to update." – Monefy

To get started, track all your expenses during the first week without setting any limits. This will help you identify your actual spending habits. Stick to 8–12 categories to keep things manageable and avoid feeling overwhelmed. If you’re budgeting as a couple, Monefy’s cloud syncing feature (via Google Drive or Dropbox) makes it easy to share envelopes. Both partners can log expenses from their phones and see updates instantly.

Another handy tool is the transfer feature, which lets you move funds between accounts - like transferring money from your checking account to a "Cash" envelope - without accidentally counting it twice. You can also add notes to specific purchases (e.g., "$150 - Car repair") to make your monthly reviews more detailed and useful.

Conclusion

Envelope budgeting sets clear spending boundaries, taking willpower out of the equation. When an envelope runs out, spending stops. This approach creates a natural checkpoint, helping you stick to your plan without feeling restricted.

It’s particularly effective for managing flexible expenses like groceries or dining out, as it forces you to make visible trade-offs. Fixed costs like rent and insurance stay consistent and are handled separately. By focusing on discretionary spending, the method encourages deliberate choices. For instance, if you move funds from one envelope to cover an unexpected expense, it forces you to evaluate and prioritize your spending.

Monefy takes this tried-and-true system and adapts it for today’s world. It combines the simplicity of traditional envelopes with the convenience of digital tools. With features like cloud syncing and secure data management, it’s perfect for modern needs - whether you’re splitting expenses with a partner, managing multiple accounts, or tracking online purchases.

To get started, create 5–8 categories targeting your biggest spending areas. Use the first month to tweak and fine-tune your envelope amounts based on your habits. This system isn’t about being flawless - it’s about aligning your money with your goals, not your impulses.

FAQs

How do I handle categories with irregular expenses?

To handle irregular expenses using envelope budgeting, set up dedicated envelopes for these costs, such as "Car Insurance," "Holiday Gifts," or "Home Repairs." Then, contribute to them consistently over time. For instance, if you expect to spend $600 on holiday gifts in December, start saving $50 a month from January. This approach spreads out the financial burden, ensuring you're ready for these expenses without straining your budget.

What should I do if I run out of money in an envelope mid-month?

If an envelope runs out of money halfway through the month, you have two options: either hold off on spending in that category until the next budget cycle, or shift funds from another envelope if your budget allows. This approach helps you stick to your financial plan and keep control over your spending.

Can I use Monefy instead of cash for envelope budgeting?

Monefy allows you to take the classic envelope budgeting approach into the digital age. Within the app, you can allocate funds to various spending categories, making it easier to manage your budget and monitor expenses. It works much like the traditional envelope system but with the convenience of modern technology.