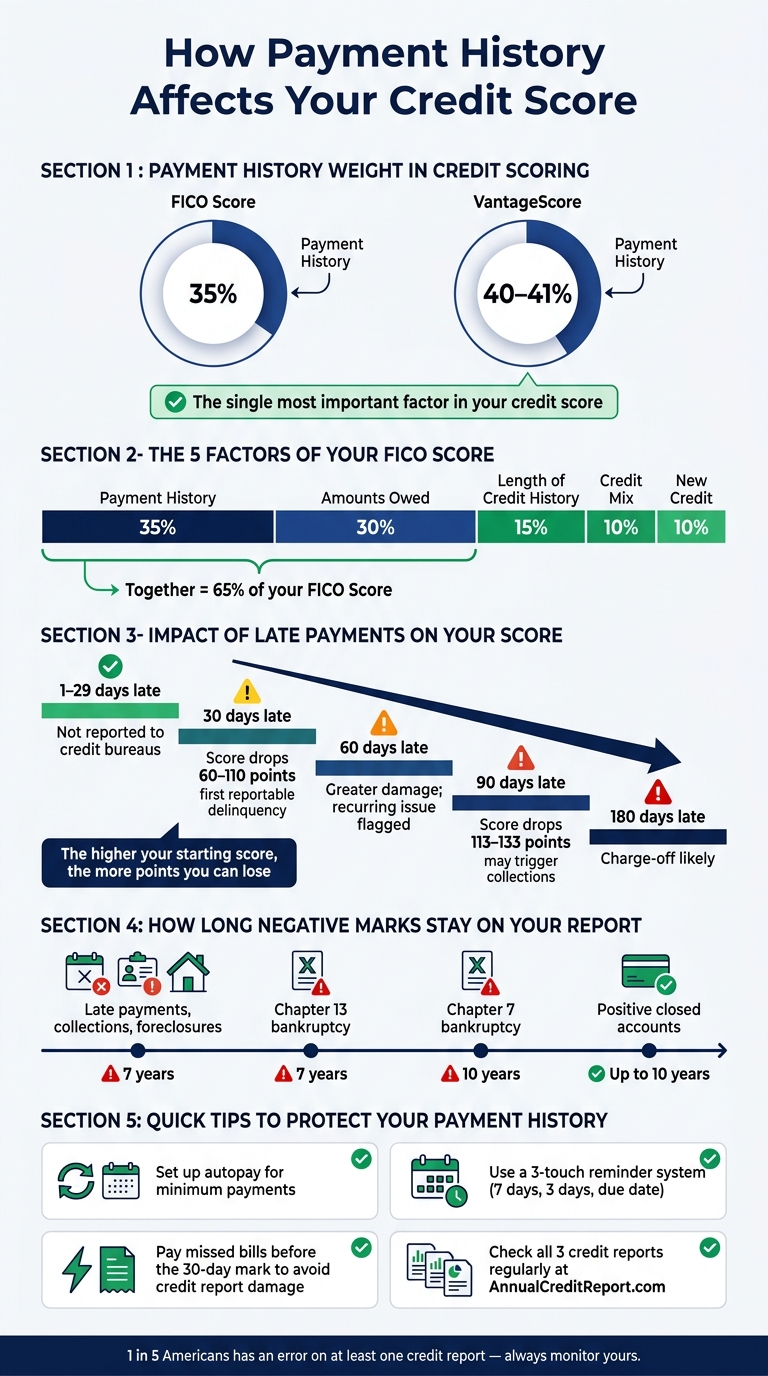

Your payment history is the single most important factor in determining your credit score, accounting for 35% of your FICO Score and up to 41% of your VantageScore. Lenders heavily rely on this data to assess your reliability in repaying debts. Even one late payment - especially if it's 30 days overdue - can drop your score by 60 to 110 points, depending on your starting score.

Key takeaways:

- What counts as payment history? Whether you pay your bills on time, how often you're late, and the severity of delays (e.g., 30, 60, or 90 days overdue).

- How long does it matter? Negative marks like late payments stay on your credit report for 7 years, but their impact diminishes over time with consistent on-time payments.

- What can you do? Use tools like autopay, set reminders, or adjust due dates to avoid missed payments. You can also track your expenses to ensure you have enough funds for every bill. If you slip up, act fast - pay before the 30-day mark to avoid credit report damage.

How Payment History Affects Your Credit Score: Key Stats & Factors

How Payment History Works in Credit Scoring Models

What Is Payment History?

Payment history is essentially a record of how reliably you've paid your credit accounts. This includes credit cards, mortgages, auto loans, student loans, and personal loans. If you've missed or delayed payments, those are noted in your credit report.

As Credit Karma puts it:

"Payment history is the section of your credit reports that shows whether you paid each reported account on time, and if not, how late you were."

Credit scoring models don't just look at whether you've paid - they also consider how late the payments were, how often you've been late, and how recently it happened. For example, a single late payment from five years ago won't weigh as heavily as repeated missed payments within the last year.

Now, let's dig into how payment history shapes your credit score.

How Much Does Payment History Affect Your Credit Score?

Payment history plays a massive role in determining your credit score. It accounts for 35% of your FICO Score and about 40% to 41% of your VantageScore. This makes it the most influential factor in your credit profile.

According to FICO:

"Track record of payment tends to be the strongest predictor of the likelihood that you'll pay all debts as agreed to."

Because 90% of lenders rely on FICO scores, your payment history directly impacts your ability to secure loans and the interest rates you'll pay.

One important note: a payment isn't marked as late on your credit report until it's at least 30 days past due. So, if you catch and pay a missed bill within that 30-day window, you can avoid potential damage to your credit score.

Other Factors That Affect Credit Scores

While payment history is the most important factor, it's not the only one. Your FICO Score is based on five components, each with a specific weight:

| Factor | Weight | What It Measures |

|---|---|---|

| Payment History | 35% | Whether payments are made on time |

| Amounts Owed | 30% | Total debt and how much of your credit limit is used |

| Length of Credit History | 15% | Age of your oldest, newest, and average accounts |

| Credit Mix | 10% | Variety of account types (e.g., loans, credit cards) |

| New Credit | 10% | Recent credit inquiries and newly opened accounts |

Together, payment history and amounts owed make up 65% of your FICO Score. These two factors demand the most attention, as they have the largest and most immediate impact. The remaining components - credit history length, credit mix, and new credit - are still worth monitoring, but they tend to evolve more slowly over time compared to the effect of making payments on time.

sbb-itb-02fd20a

What Lenders Look at in Your Payment History

When lenders check your credit report, they dig deeper than just confirming if you’ve paid your bills. They’re searching for patterns in how you handle payments. Both lenders and credit scoring models focus on how consistently you pay on time and take a close look at any late payments, evaluating them based on recency, severity, and frequency.

Key Data Points in Payment History

Your payment history covers a range of account types. For each account, lenders assess your record of on-time payments and scrutinize specific issues like late payments (often categorized by how many days they’re overdue), collections, charge-offs, and public records such as bankruptcies or foreclosures.

Late payments are broken into tiers, and each tier has a progressively larger impact:

| Days Past Due | Status |

|---|---|

| 1–29 days | Typically not reported to credit bureaus, though late fees may apply |

| 30 days | The first reportable delinquency, leading to a noticeable score drop |

| 60 days | Indicates a recurring issue, with greater credit score damage |

| 90 days | A critical marker that may trigger collection actions |

| 180 days | Often results in a charge-off |

The jump from being 30 days late to 90 days late can be especially costly. For instance, FICO Score 9 simulations show that someone with a starting score of 793 could lose 63–83 points from a single 30-day late payment. But if that payment stretches to 90 days overdue, the score drop could range from 113 to 133 points. That kind of drop might take you from excellent credit to missing out on a competitive mortgage rate. If you're struggling to manage your debt, financial advisors can help you create a plan to improve your standing.

"A recent late payment could be more damaging to your score than a number of late payments that happened a long time ago." - myFICO

Lenders also take note of how long these negative marks remain on your credit report.

How Long Does Payment History Stay on Your Credit Report?

Lenders don’t just look at the details - they also consider how long those details stick around. Most negative items, like late payments, collections, and foreclosures, stay on your credit report for seven years from the date of the original delinquency. Bankruptcies, however, have a longer shelf life: Chapter 13 bankruptcies typically stay for seven years, while Chapter 7 bankruptcies remain for ten years. On the bright side, closed accounts with a positive history can benefit your credit score for up to ten years.

Over time, consistently paying on time helps offset the impact of older negative marks.

The Role of the Three Credit Bureaus

Equifax, Experian, and TransUnion are the three major credit bureaus that independently collect payment data from different types of banks and creditors, usually on a billing cycle basis. Since not all lenders report to all three bureaus, your payment history might differ slightly across reports. That’s why it’s smart to check all three regularly - an error on one report won’t automatically fix itself.

Common Payment History Problems and How They Hurt Your Score

A single mistake in your payment history can have lasting consequences. The impact depends on what occurred, how recent it was, and its severity. Grasping these details is crucial for improving your credit profile, as discussed in the next section.

Late Payments and Delinquencies

Missing a payment by 30 days or more can cause immediate and significant damage to your credit score. Ted Rossman, Senior Industry Analyst at Bankrate, explains:

"The bigger they are, the harder they fall. If your score is near perfect, you could lose 100 points or more because of a single 30-day delinquency."

This is supported by FICO Score 9 simulations. For example, Maria, who started with a score of 793, lost 63–83 points from one 30-day late payment. Meanwhile, Sophia, with a starting score of 607, saw a smaller drop of 17–37 points for the same infraction. Essentially, the higher your score, the more you stand to lose.

The situation worsens as the delinquency progresses. When Maria's late payment extended to 90 days, her score dropped by 113–133 points - nearly double the impact of the initial 30-day delinquency. At this stage, lenders often view the account as a significant default risk.

Major Negative Events

Beyond late payments, more severe issues like charge-offs, collections, bankruptcies, and foreclosures can wreak havoc on your credit score. These are considered major red flags by lenders and scoring models.

- Charge-offs occur when a lender writes off your debt as a loss, typically after 180 days of non-payment. This signals that the creditor has stopped trying to collect the debt.

- Collections happen when an unpaid account is handed over to a third-party agency, creating a separate negative entry on your report. Even if you pay the balance later, these accounts cannot return to "current" status.

- Bankruptcies are the most severe. Chapter 13 bankruptcies remain on your credit report for seven years, while Chapter 7 stays for ten years.

How Recency and Severity Shape the Impact of Negative Marks

The timing of a negative mark is just as important as its severity. Scoring models place more weight on recent behavior than on older events.

For instance, a late payment remains on your report for seven years, but its effect starts to diminish after about two years - provided you maintain consistent on-time payments moving forward. While the negative mark won't disappear immediately, its influence fades over time, allowing your score to recover gradually.

How to Build and Maintain a Positive Payment History

Keeping a strong payment history boils down to consistency and good habits. By sticking to a few smart strategies, you can ensure your payments are always on time.

As Firstcard explains:

"Payment history is the biggest lever you control, and the good news is that protecting it is mostly about habits, not money."

How to Make On-Time Payments Consistently

One of the easiest ways to avoid late payments is by setting up autopay for at least the minimum amount due on all your accounts. This ensures your payments are made even if life gets hectic. To make it more effective, schedule autopay for 2–3 days after your paycheck hits your account. This gives you a cushion for any processing delays and reduces the risk of overdrafts.

If you prefer manual payments, try a "three-touch" reminder system. Set a calendar alert seven days before the due date, send yourself an email three days ahead, and leave a note for the actual due date. Another tip: record due dates a few days early in your calendar to give yourself extra breathing room.

You can also adjust due dates to align better with your pay schedule. For instance, if multiple bills - like rent, your car loan, and credit card payments - are due in the same week, contact your creditors and request new dates. This small tweak can help smooth out cash flow issues.

Despite your best efforts, if you miss a payment, there are steps you can take to reduce the impact.

What to Do If You Miss a Payment

If a payment slips through the cracks, act fast. Make the payment - or at least the minimum amount - before it hits the 30-day late mark. This prevents it from appearing on your credit report, even if you have to pay a late fee.

If the payment is already overdue, settle the balance as soon as possible. Credit scores take bigger hits with each 30-day increment of lateness, so stopping the damage early is key. Once you're caught up, consider contacting your creditor to request a goodwill adjustment. This works best if you have a solid history of on-time payments and the missed payment was a one-time mistake. If you're dealing with ongoing financial difficulties, ask about hardship programs. These programs may offer benefits like fee waivers, lower interest rates, or temporary payment relief.

In addition to addressing missed payments, a strong budget can help you stay on track moving forward.

Budgeting to Stay on Top of Payments

Many people underestimate their spending by 20–30% when relying on memory. This gap can lead to missed payments - not because you don't earn enough, but because it's easy to lose track of where your money goes.

Tracking your daily expenses can help close that gap. Studies show that simply being aware of your spending can cut costs by 15–25% in the first month. That saved money can then go toward covering your bills. Apps like Monefy make it simple to log income and expenses across multiple accounts. Its clear visual interface lets you see at a glance whether you have enough set aside for upcoming payments. Plus, features like customizable reminders and multi-device syncing are great for households managing shared finances.

To complement expense tracking, consider following the 50/30/20 rule. This budgeting method divides your income into three categories: 50% for essentials (like housing, utilities, and minimum debt payments), 30% for discretionary spending, and 20% for savings. By treating recurring bill payments as fixed expenses, you can build the rest of your spending plan around what's left over.

How to Monitor Your Payment History Over Time

Keeping an eye on your credit reports is just as important as making on-time payments. Monitoring your credit helps you maintain a strong payment history while catching potential errors. Did you know that 1 in 5 Americans has an error on at least one of their three credit reports?. Even a single mistake, like an incorrectly reported late payment, can cause your score to drop by 50 to 100 points. Spotting these issues early can save you from unnecessary damage to your credit.

How to Check Your Credit Reports

The best place to access your credit reports is AnnualCreditReport.com, the only federally approved site for free reports from Equifax, Experian, and TransUnion. You can get a report from each bureau weekly without any cost. Plus, checking your own credit report is considered a "soft inquiry", so it won’t affect your credit score at all.

For ongoing credit health monitoring, space out your checks throughout the year. For instance, review Equifax in January, Experian in May, and TransUnion in September. If you're gearing up for a major loan, like a mortgage, check all three reports three to six months in advance. This gives you enough time to address any potential issues.

"Your credit report isn't just a snapshot... it's a documented financial reputation that follows you through major life decisions." - Troy Johnston, Founder, StackEasy.ai

After reviewing your report, take immediate action to resolve any discrepancies using the steps outlined below.

How to Dispute Errors on Your Credit Report

If you find an error - such as a payment incorrectly marked as late - you have the right to dispute it for free under the Fair Credit Reporting Act (FCRA). Credit bureaus are legally required to investigate and respond, usually within 30 days.

To dispute an error, contact both the credit bureau and the original creditor. Provide supporting documents like bank statements, emails, or canceled checks to strengthen your case. Reaching out to both parties helps ensure the error isn’t re-reported after the bureau corrects it.

"A well-documented dispute file is your most powerful tool. It transforms your claim from a simple complaint into a formal, evidence-backed challenge." - Ginsburg Law Group

If you’re sending your dispute by mail, use certified mail with return receipt requested. This creates a legal trail and officially starts the 30-day investigation clock. Always send copies of your documents, not the originals.

Tracking Your Credit Health Long-Term

Regular monitoring is key to maintaining stable credit over time. Make it part of your financial routine. Pay special attention to the personal information section of your reports - unfamiliar addresses or misspelled names could signal identity theft.

Using tools like Monefy can help you connect your spending habits with your credit goals. When you track your expenses consistently, you’re more likely to cover bills on time, which is the foundation of a clean payment history. Building strong credit isn’t about short-term wins; it’s about aligning your daily habits with your long-term financial goals.

Conclusion: Take Control of Your Payment History

Your payment history plays a bigger role in shaping your credit score than any other factor. The upside? It's also something you have the power to manage with the right habits.

Small, consistent actions can make a huge difference. As mentioned earlier, even one 30-day late payment can knock your score down by dozens of points - but you can avoid that. Use tools like automated payments, timely reminders, or apps like Monefy to stay on top of your bills. If a payment does slip through the cracks, address it quickly - before it hits that 30-day mark. And if you've built a solid history with a creditor, a goodwill letter might help repair the situation.

Understanding your monthly cash flow is the key to staying in control. When you know exactly where your money is going, you're less likely to be blindsided by a due date. Building these habits now can help ensure lasting credit strength.

Great credit is built on consistent, on-time payments. Start today by taking one simple step - set up autopay, check your credit report, or use Monefy to organize your budget. Each on-time payment brings you closer to a more secure financial future.

FAQs

Will paying a bill a few days late hurt my credit score?

Paying a bill a few days late usually won’t hurt your credit score. That’s because creditors typically report late payments to major credit bureaus only after they’re 30 or more days overdue. However, you could still face late fees, which can add up over time. Since your payment history plays a major role in determining your credit score, staying on top of due dates is crucial. Tools like Monefy can help by letting you track expenses and manage budgets, making it easier to pay bills on time and maintain better financial habits.

How can I rebuild my score after a late payment?

If you've missed a payment, the best way to start rebuilding your credit score is to bring the account current as soon as possible. From there, focus on consistently paying on time. Late payments do stick around on your credit report for seven years, but they hurt your score less as time passes - especially after the first two years.

To stay on top of your payments and avoid future issues:

- Pay at least the minimum amount due every month.

- Set up automatic payments or payment reminders to avoid forgetting deadlines.

- Regularly check your credit reports to spot any inaccuracies or changes.

- Hold off on opening unnecessary new accounts, as this could further impact your score.

Consistency and careful management are key to bouncing back.

What should I do if my credit report shows a late payment by mistake?

If you spot an incorrect late payment on your credit report, you have the right to dispute it at no cost. Start by reaching out to both the credit bureau and the creditor. Submit a written request that clearly explains the mistake and back it up with supporting documents, such as bank statements or payment confirmations. Once you file the dispute, they are required to investigate - usually within 30 days - and fix or remove the inaccurate information if your claim is found to be valid.