Savings apps simplify saving by automating transfers, tracking spending, and helping you set financial goals. They use features like round-ups, scheduled transfers, and AI-driven smart savings to make saving easier, especially for users with unpredictable cash flow. Research shows automation, particularly fixed savings rules tied to income, can significantly boost savings. However, their effectiveness depends on user commitment, and they come with potential drawbacks like privacy concerns and overreliance on automation.

Key Takeaways:

- Automation Works: Scheduled transfers lead to 1.5–3.5x higher savings than round-ups.

- Goal Setting Helps: Users with multiple savings goals save more.

- Privacy Risks Exist: Sharing financial data may expose you to risks.

- Commitment is Key: Apps are tools, not solutions; consistent habits matter.

Savings apps can be a valuable tool for building financial discipline, but they work best when paired with active engagement and careful monitoring.

How Savings Apps Work

Comparison of Savings App Methods: Round-Ups vs Scheduled Transfers vs Smart Transfers

Savings apps simplify the process of saving money by combining automation, data analysis, and behavioral psychology. Instead of relying on willpower to save manually, these apps connect to your bank accounts and move money automatically based on preset rules - or even rules the app determines for you. The idea is straightforward: make saving effortless so you can grow your wealth without constantly thinking about it. Let’s explore the specific methods these apps use.

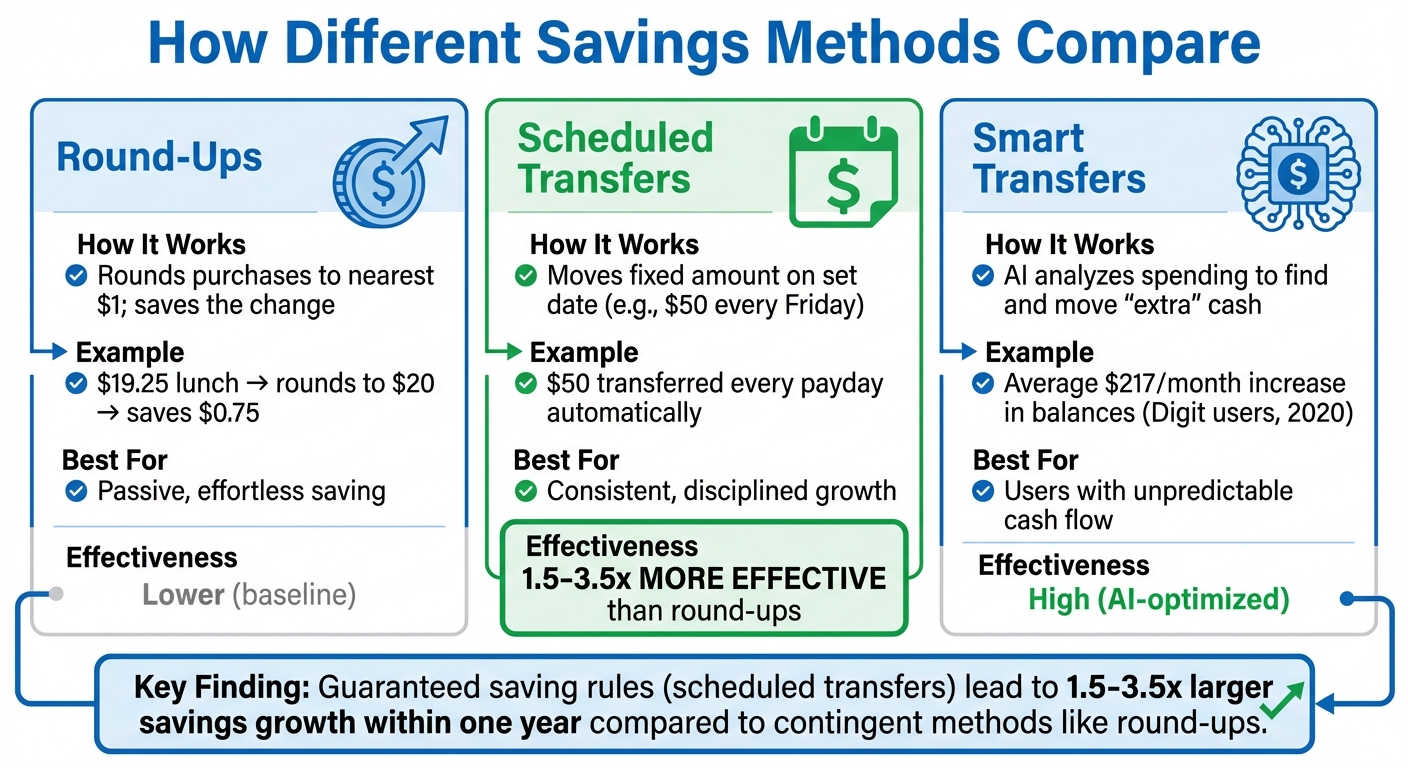

Most savings apps operate using one of three main strategies: automated recurring transfers, round-up features, or smart algorithmic transfers. Automated recurring transfers allow you to set a fixed amount and schedule, like transferring $50 from your checking to savings account every Friday. Round-up features link to your debit or credit card, rounding each purchase to the nearest dollar and saving the spare change. For example, buying groceries for $87.45 would result in $0.55 being transferred to savings. Smart transfers take automation further by using AI to analyze your income and spending habits, then moving small, expendable amounts into savings without you lifting a finger.

Many apps also let you create goal-based buckets (sometimes called "envelopes") for specific targets such as vacations, emergency funds, or a down payment. This taps into the psychological principle of mental accounting, which helps you resist spending money set aside for a specific purpose. Research shows that users who set multiple savings goals saved an average of $114 more over five months compared to those with just one goal. Some apps even offer direct deposit splitting, where a portion of your paycheck is automatically routed into savings before it reaches your checking account.

Automated Transfers and Round-Up Features

Two of the most popular automation methods are round-ups and scheduled transfers, though they function quite differently. Round-ups are tied to spending: they save money only when you make a purchase. For instance, if you spend $19.25 on lunch, the app rounds it to $20, saving $0.75. Once the total round-up amount hits $5, it gets transferred to your savings or investment account. This method is effortless and works in the background.

Scheduled transfers, by contrast, are consistent and predictable. They move a fixed amount of money on a set date, regardless of your spending patterns. Studies show that guaranteed saving rules, like scheduled transfers, lead to savings growth that is 1.5 to 3.5 times larger within a year compared to contingent methods like round-ups. The Consumer Financial Protection Bureau emphasizes this approach:

"Building towards your savings goals can take time and dedication, but regularly putting money into savings - even small amounts - is the best way to see your money grow".

Another option is smart transfers, where AI evaluates your cash flow and moves small amounts of surplus money into savings automatically. For example, users of the app Digit who joined in June 2020 saw an average increase of $217 per month in their account balances thanks to this feature.

| Feature Type | How It Works | Best For |

|---|---|---|

| Round-Ups | Rounds purchases to the nearest $1; saves the change. | Passive, effortless saving. |

| Scheduled Transfers | Moves a fixed amount on a set date (e.g., $50 every Friday). | Consistent, disciplined growth. |

| Smart Transfers | AI analyzes spending to find and move "extra" cash. | Users with unpredictable cash flow. |

Expense Tracking and Budget Management

Savings apps don’t just help you save; they also give you a clear picture of where your money is going. By linking to your bank accounts, these tools automatically categorize your expenses - groceries, utilities, dining out, and more - making it easier to spot unnecessary spending. This visibility can have a big impact. A study led by Bruce Carlin at Rice Business tracked 13,411 users of a financial aggregator app in Iceland between 2011 and 2017. After 12 months, individuals reduced non-sufficient funds (NSF) fees by 14.1%, and after two years, the reduction jumped to 38.4%. Carlin explained:

"When people have a clearer picture of their finances, they can make better decisions. And when fintech companies build tools that prioritize accessibility and ease of use, they're not just creating products - they're helping improve financial outcomes".

Automatic categorization also saves time, eliminating the need for manual tracking, which 53.8% of budgeters still rely on. Many apps provide real-time updates on your "safe-to-spend" money in each category, helping you avoid overspending. Zach Whelchel, Founder of MyBudgetCoach, highlights the value of this approach:

"These apps help you give every dollar a job before you spend the money. Learning to live by your budget helps you align your spending to your values".

Nearly 80% of budgeting app users check their apps weekly, and 29.9% engage daily. Moreover, over 88% of users find these tools "very helpful" or "extremely helpful".

Goal-Setting and Progress Tracking

Savings apps also excel at helping users set and track financial goals. Whether you’re building an emergency fund, saving for a vacation, or working toward a down payment, these tools let you define specific objectives and monitor your progress through visual aids like progress bars or "bubble budgets." By syncing with your bank accounts, the apps automatically update your progress as transactions occur, offering a complete view of your finances. This approach is motivating: 45% of people who follow a budget say that setting financial goals is a key part of their strategy.

Many apps also include alerts and reminders to keep you on track and ensure you hit your milestones. Kara Robinson, a financial expert, notes:

"By setting up goals on financial apps, users can stay on top of their progress. This boosts motivation, and it's very satisfying to see a savings account balance increase or a debt account decrease each month".

The use of mental accounting - separating funds into specific "buckets" - prevents accidental overspending on money earmarked for particular purposes. This method is highly effective, with users employing guaranteed saving rules significantly more likely to reach milestones like saving $500 or $1,000 within a year.

Benefits of Using Savings Apps

Savings apps bring more to the table than just convenience - they transform how you manage your money. By minimizing effort, improving transparency, and keeping your financial goals front and center, these tools make saving easier and more effective. Through automation, real-time updates, and insights from behavioral finance, they help you build wealth without constant manual effort.

Convenience and Automation

One standout advantage of savings apps is how they remove the need to consciously remember to save. Instead of relying on willpower, these apps automate the process - whether through scheduled transfers, round-ups on purchases, or algorithms that analyze your cash flow. As Bruce Carlin, Professor of Finance at Rice Business, explains:

"When checking your balance becomes as easy as checking social media, you're more likely to do it."

Many of these apps also streamline your finances by consolidating multiple accounts into a single dashboard. They automatically categorize transactions and send real-time alerts for due bills or low balances, helping you avoid costly overdraft fees (which affected about 25% of U.S. consumers in 2023). This automation not only simplifies saving but also gives you a clearer picture of your financial health.

Gaining Better Insight Into Your Finances

When your finances are organized and easy to track, making smarter spending decisions becomes much simpler. Savings apps categorize your transactions automatically, making it easier to spot recurring expenses you could reduce. Real-time updates help you stay within your budget by calculating a "safe-to-spend" amount that factors in upcoming bills and savings goals.

Real-Time Goal Tracking

With a clearer understanding of your spending, you can focus on specific financial goals and monitor progress in real time. Many savings apps allow you to create separate "buckets" for different objectives - like an emergency fund, a vacation, or a down payment - and automatically update your progress as you save. This method leverages mental accounting, making it easier to resist the temptation to dip into funds set aside for specific purposes.

Visual tools like progress bars and milestone notifications make saving feel more engaging. Some apps even use gamification, offering badges or levels to celebrate achievements. Real-time alerts also help you avoid overspending. As money-saving expert Andrea Woroch points out:

"Many savings apps automatically categorize expenses into preset spending categories and alert you when you're close to exceeding your limits, ensuring you stick to your budget and goals."

Research backs this up: nearly 80% of budgeting app users check their apps weekly, 29.9% use them daily, and over 88% find these tools very or extremely helpful.

Drawbacks and Limitations

While savings apps bring convenience and benefits, they also come with their own set of challenges. Being aware of these limitations can help you use them wisely and avoid potential issues.

Privacy and Security Concerns

Connecting a savings app to your bank account means sharing sensitive financial data, and this comes with risks. Many apps share user information with third-party partners for targeted advertising and marketing, often going beyond what's necessary for their core services. For instance, 57% of U.S. adults are concerned about banks sharing financial data without notifying them, and 76% believe banks should get explicit permission before sharing such data with other companies.

Fraud is another concern. One in three U.S. banking customers reported being victims of fraud, such as unauthorized card use, within a single year. The risks increase if your device, which has access to financial accounts, is lost or stolen. Alarmingly, only half of the major banking apps reviewed by Consumer Reports give users the option to turn off targeted advertising within the app.

To protect your data, take these steps:

- Enable two-factor authentication and use biometric logins.

- Adjust your phone's privacy settings to block unnecessary app permissions, like location tracking or microphone access.

- Know how to remotely wipe your device if it's lost or stolen.

- Cancel and delete your account within the app itself - simply deleting the app from your phone won’t stop data collection.

Learning Curve for New Users

Starting with a savings app can feel daunting, especially when navigating its many features and settings. As Michelle Taylor, Founder of Women in Wealth Initiative, suggests:

"This will help keep you on track and prevent you from feeling overwhelmed by multiple features".

Privacy settings can also be tricky for beginners. Many apps default to sharing user data with third parties for marketing purposes, which can be hard to spot. Christina Tetreault, Senior Policy Counsel at Consumer Reports, notes:

"These companies all claim to offer personalized services, but that's not what you'll see in the fine print. There's a big disconnect".

Additionally, some apps promise "personalized advice" but include disclaimers that they aren’t responsible for its accuracy or relevance.

To ease into using a savings app, take advantage of free trials - many apps offer 30-day trials to help you decide if the interface works for you. Right after setup, review and adjust privacy settings to limit permissions and opt out of targeted advertising.

Overreliance on Automation

Automation is a double-edged sword. While it simplifies saving, it can also lead to complacency. If you rely too heavily on automated tools, you might stop actively monitoring your finances. Casey Newmeyer, Assistant Professor of Marketing at Case Western Reserve University, explains:

"If you're unable to save on your own, these tools can at best act as a bandage".

He further warns:

"It's counterintuitive, but these tools can be detrimental if they make users miss opportunities and pay less attention to finances than they otherwise might".

Automation errors, like miscalculating cash flow, can result in overdraft fees. These tools work best when paired with a strong commitment to saving. As Melissa Murphy Pavone, a Certified Financial Planner, puts it:

"Money-saving apps are only as effective as your commitment to using them".

To avoid pitfalls, regularly review your automation settings to ensure they align with your financial goals. And, most importantly, focus on developing solid money management habits outside of any app.

sbb-itb-02fd20a

Evidence of Effectiveness

Research shows that savings apps can improve financial outcomes when used thoughtfully and strategically.

How Automation Affects Behavior

Automation tackles a common psychological hurdle called present bias - the tendency to prioritize immediate desires over future needs. By automating the saving process, these apps ensure money gets set aside before you even have the chance to spend it.

But not all automation methods work the same way. A December 2022 report from the Consumer Financial Protection Bureau analyzed data from the app Qapital and found that guaranteed saving rules - like automatic transfers on payday - were far more effective. Users relying on these rules were 1.5 to 3.5 times more likely to hit savings milestones of $500 or $1,000 within a year compared to those using contingent rules, such as round-ups. The difference between these approaches is significant.

Here’s why: guaranteed rules tie savings to your income, ensuring consistent deposits regardless of spending habits. In contrast, round-ups depend on transaction activity, typically moving only small amounts based on your purchases.

These insights highlight why automation, especially income-based automation, can make a big difference for savers.

User Success Stories

Real-world data backs up the benefits of automation. A June 2020 study by the Financial Health Network looked at new users of the Digit app and found that active users boosted their balances by an average of $217 per month through automated transfers.

Interestingly, the study uncovered another key finding: people who set multiple savings goals saved more than those with just one. Over their first five months, users with multiple goals deposited $114 more than single-goal users - $91 more through automated transfers and $37 more through manual deposits. Each additional goal added an average of $79 in total deposits over five months.

This phenomenon, known as the mental accounting effect, shows that labeling money for specific purposes - like "Emergency Fund" or "Vacation" - encourages people to save more than if they lumped it all into one general fund. The study controlled for outside factors, such as stimulus payments, confirming that the app itself was the driving force behind these improvements.

How Monefy Helps You Save

Monefy takes the concepts of automation and goal-setting and turns them into practical tools to help you manage your finances more effectively. By combining these strategies with a user-friendly design and strong security, Monefy makes personal finance management simpler and more efficient.

Expense and Income Tracking

Monefy simplifies tracking your finances by automatically recording your income and expenses. It categorizes transactions - like groceries, bills, or recreation - so you can see exactly where your money is going. This detailed breakdown helps you identify recurring costs and uncover spending habits you might not have noticed.

The app also provides updates on whether you're sticking to your budget or spending more than planned. This kind of transparency can make all the difference when you're trying to make smarter financial decisions.

Customizable Budgets and Financial Goals

With Monefy, you can tailor your budget to fit your personal goals, whether that's building an emergency fund, paying off debt, or saving for a big purchase like a home. You can even set visual checkpoints to keep yourself motivated. The app allows you to customize categories for expenses, income, and savings, so your budget reflects your unique lifestyle and spending patterns.

Monefy also makes goal-setting easier by breaking down larger financial objectives into smaller, achievable milestones. This approach not only keeps you organized but also helps you stay motivated as you see steady progress toward your goals.

Secure and Easy-to-Use Design

Your financial data is safe with Monefy, thanks to features like bank-level encryption and multi-factor authentication. Plus, the app is designed for simplicity, making it easy to navigate and adjust as needed. A survey from Academy Bank highlights the importance of user-friendly design:

"A clean, intuitive interface can make or break a budgeting app - and according to our survey respondents, it's the most important feature of all".

In fact, over 88% of users say budgeting apps and digital tools are either "very helpful" or "extremely helpful". Monefy’s straightforward interface aligns with this feedback, making it easier for users to stay engaged and committed to their financial goals.

Conclusion: Are Savings Apps Worth Using?

Savings apps can offer genuine advantages, but their effectiveness depends on how you use them. Research highlights that fixed saving rules - like scheduling automatic transfers on payday - can lead to a 1.5 to 3.5 times greater increase in the highest amount saved over a year compared to more flexible options like round-ups.

The key to success with these apps lies in consistency. Tools like Monefy work best when they complement habits you're already developing, rather than acting as a one-stop solution.

Before diving in, identify your financial priorities. Are you looking to monitor your spending, or do you need a simple way to save for specific goals? Michelle Taylor, Founder of Women in Wealth Initiative, offers this advice:

"It's important to figure out what you want from a financial app before picking one... this will help keep you on track and prevent you from feeling overwhelmed with choices".

It's also important to weigh the pros and cons. Automation can be a lifesaver, particularly for those working to build emergency savings on a tight budget. However, consider potential downsides like fees, data privacy risks, and the lack of personalized support.

FAQs

How do savings apps protect my financial information?

Savings apps take protecting your financial data seriously, using a variety of advanced security measures. For starters, they often implement encryption protocols, which ensure your data remains secure while being transferred and shield it from any unauthorized access. On top of that, many apps rely on multi-factor authentication (MFA) to add an extra layer of security by verifying your identity before granting access.

Trusted apps also adhere to strict privacy laws, such as GDPR or CCPA, to manage your data responsibly and ethically. To further safeguard your information, you can adopt simple but effective habits like creating strong, unique passwords and keeping your app updated. Apps like Monefy integrate these protections to help keep your sensitive information secure.

What are the risks of relying too much on automated savings apps?

While savings apps can be great for keeping your finances in check, leaning too much on automation has its downsides. For example, automation might give you a false sense of security, making you feel like your savings are on track without actually keeping an eye on your spending or adjusting your habits. Plus, these apps tend to work best for people with tighter budgets and might not meet the needs of higher-income individuals or those managing more complex financial goals.

The key is to treat these tools as part of your strategy - not the whole solution. Pairing automation with regular check-ins on your spending, saving, and budgeting habits is essential. By staying involved in your financial decisions, you can ensure you're moving toward your goals while staying flexible enough to handle any changes life throws your way.

How can I use savings apps to reach multiple financial goals?

Savings apps can be incredibly useful for tackling a variety of financial goals, provided you use them wisely. Start by identifying what you want to achieve - whether it’s building an emergency fund, saving for a dream vacation, or knocking out debt. Many apps make saving effortless by automating the process. For instance, you can set rules to round up your purchases or schedule regular transfers, so saving becomes a habit without requiring constant attention.

Take Monefy, for example. This app helps you track your income, spending, and overall savings progress all in one place. You can even create customized savings rules tailored to each of your goals, ensuring your money is allocated based on what matters most to you. Reviewing your progress regularly and tweaking your approach as needed can keep you on the right path and help you make the most out of your efforts.

Consistency and automation are your best allies here. By minimizing the need for willpower and aligning your strategy with your financial priorities, you can effectively work toward multiple goals simultaneously.