Rebuilding your emergency savings doesn’t have to feel overwhelming. Start small and focus on these five practical steps to get back on track:

- Automate Your Savings: Set up automatic transfers from your paycheck to a dedicated savings account. Even small contributions, like $10 or $50 per paycheck, can grow over time. Use high-yield savings accounts (HYSAs) offering 3.30%–4.00% APY to maximize growth.

- Cut Non-Essential Spending: Track your expenses using tools like Monefy to identify and reduce unnecessary purchases. Small daily savings, such as $1–$3, can add up significantly over time.

- Redirect Windfalls: Use tax refunds and cash-back rewards to boost your savings. A $3,000 tax refund, for example, can quickly cover a significant portion of your emergency fund goal.

- Earn Extra Income: Take on side gigs, like freelancing or food delivery, to accelerate savings. Even earning $100 a month can add $1,200 to your fund in a year.

- Open a High-Yield Savings Account: Keep your emergency fund in a separate HYSA to earn more interest while maintaining easy access. Rates as of February 2026 range from 3.30% to 4.35%.

Start small and stay consistent. Prioritize automation, mindful spending, and leveraging extra income or windfalls to hit milestones like $500, $1,000, and eventually 3–6 months of living expenses.

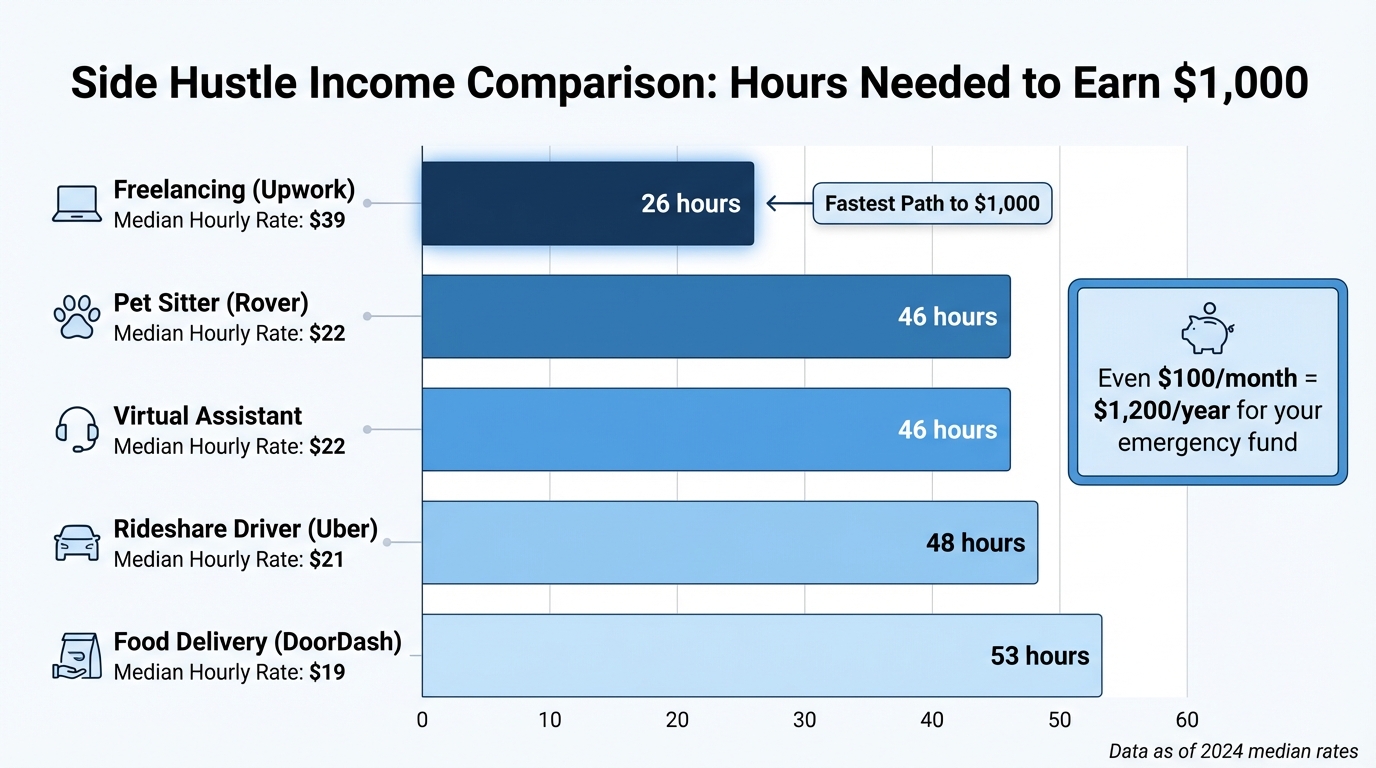

Side Hustle Income Comparison: Hours Needed to Earn $1,000

1. Set Up Automatic Transfers from Your Paycheck

Automating your savings is a smart way to rebuild your emergency fund without overthinking it. By setting up automatic transfers from your paycheck, you ensure money is saved before it can be spent elsewhere.

Many U.S. employers let you divide your direct deposit between multiple accounts. All you need to do is give your HR or payroll department the routing and account numbers for your savings account. Then, decide whether a fixed dollar amount or a percentage of each paycheck goes straight into that account. Financial planner Jeremy Zuke from Abundo Wealth emphasizes:

"I strongly recommend automating your monthly contribution because when you never see the money, it's easier to avoid accidentally spending it."

If your employer doesn’t offer split deposits, don’t worry. Most banks allow you to schedule recurring transfers through their apps or websites, making payday transfers just as easy.

Why Automation Speeds Up Savings

The beauty of automation lies in its consistency. Even small amounts - like $10 or $50 per month - can accumulate over time and make a big difference.

To make your savings grow even faster, consider using a high-yield savings account (HYSA). For example, as of February 2, 2026, Bread Financial offers a 4.00% APY, Forbright Bank provides 3.85% APY, and Marcus by Goldman Sachs offers 3.65% APY. These rates are 7 to 10 times higher than the average for traditional savings accounts, meaning your money works harder for you without any extra effort.

Simple to Set Up

Getting started is easier than you might think. For employer-based transfers, you just need your savings account’s routing and account numbers, which you can find through your bank’s app or website. If you’re doing bank-to-bank transfers, most financial institutions let you link accounts and schedule recurring transfers right from their mobile platforms.

Timing your transfer to align with payday ensures your savings are secured before you even think about spending. This simple step creates a solid foundation for better financial habits.

Building a Lasting Savings Routine

One of the best parts of automation is that it removes the need to make monthly decisions. Treating your emergency fund contribution like any other recurring bill helps you save consistently without relying on willpower or memory.

The Consumer Financial Protection Bureau highlights this approach:

"Setting up an automatic saving program can be one of the easiest and most effective ways to get started with a new savings habit."

2. Track and Reduce Non-Essential Spending with Monefy

After automating your savings, the next step is understanding where your money goes. Many people are surprised to find they’re spending hundreds of dollars monthly on non-essentials - things like unused subscriptions, frequent takeout, or impulse buys. These expenses could instead help grow your emergency fund.

Effectiveness in Accelerating Savings Growth

Monefy’s real-time tracking makes it easy to see exactly how your spending breaks down, categorizing expenses into "needs" and "wants." This clarity helps you spot areas to cut back. Even small changes - like saving just $1 a day - can add up to $365 in a year. Bigger adjustments, like planning meals ahead, buying in bulk, or using curbside pickup to avoid impulse purchases, can reduce grocery bills by 30–40%, potentially saving over $1,800 annually. With this insight, you can make smarter, faster adjustments to your spending habits.

Ease of Implementation

Getting started with Monefy is a breeze. Its clean, user-friendly interface organizes spending into 5–7 main categories, making it easy to track without feeling overwhelmed. For even simpler management, try the "one number" budget method: total your monthly variable expenses (like groceries, gas, and entertainment), divide by 30.4, and use that amount as your daily spending limit. Setting a daily reminder - say, at 9 PM - can help you log expenses consistently without needing to monitor your spending all day.

Potential for Long-Term Financial Habits

Monefy encourages financial discipline by providing instant, real-time feedback on your spending. Many users report that seeing their balance decrease motivates them to adjust their habits quickly. With over 11 million downloads and an impressive 4.7/5 average rating from more than 283,000 reviews, the app has earned its reputation. As one loyal user shared:

"The best app for keeping track of finances. I've been using it for almost 7 years." – Ayperi, App Store

The secret to building long-term savings is consistency. Start by sticking to your daily spending limit and, over time, try trimming it by $1–$3 per day. Any leftover amount can be transferred directly into a high-yield savings account, giving your emergency fund an extra boost.

3. Direct Tax Refunds and Cash-Back Rewards to Savings

Redirecting tax refunds and cash-back rewards can give your savings a noticeable boost, especially when paired with automated transfers and spending oversight.

Effectiveness in Accelerating Savings Growth

For many, a tax refund is the largest check they receive all year. Instead of viewing it as extra spending money, consider depositing it straight into your emergency fund. For instance, a $3,000 tax refund can shave over a year off your savings timeline if you’re working toward a $9,000 goal by saving $200 a month.

Cash-back rewards can also make a difference. The average cardholder earns $278 annually, while some top-tier cards can yield up to $553 in the first year. By funneling these rewards into your savings rather than spending them, you’re essentially giving yourself a bonus every time you shop.

These strategies work hand-in-hand with automated savings and expense tracking, speeding up the growth of your emergency fund.

Ease of Implementation

Because tax refunds and cash-back rewards aren’t part of your regular budget, saving them feels effortless. As Navy Federal Credit Union puts it:

"Since this money isn't part of your typical spending, it's easy to use it for saving without missing it."

The IRS even allows you to split your tax refund, sending part of it directly into a savings account. Similarly, many credit cards and apps make it simple to redirect cash-back earnings into linked savings accounts, eliminating the need for manual transfers.

Relevance to U.S. Financial Tools and Systems

To maximize your savings, consider depositing these extra funds into a high-yield savings account. As of February 2, 2026, digital banks are offering competitive rates between 3.30% and 4.00% APY. For example:

- Bread Financial: 4.00%

- Forbright Bank: 3.85%

- Marcus by Goldman Sachs: 3.65%

- Capital One: 3.30%

Keeping your emergency fund separate from your checking account also helps avoid the temptation to dip into it impulsively. This small step can make a big difference in staying on track with your financial goals.

sbb-itb-02fd20a

4. Earn Extra Income Through Side Work

Building your emergency fund can get a serious boost by taking on side work. Even earning an extra $100 a month from occasional gigs can add up to $1,200 in a year - a solid cushion to fall back on. The trick is to find work that fits your skills and schedule while committing every dollar to savings.

Effectiveness in Accelerating Savings Growth

Not all side gigs pay the same, so choosing wisely can make a big difference. For instance, freelancing on platforms like Upwork offers a median hourly rate of $39, meaning it takes just 26 hours to save $1,000. Compare that to food delivery through DoorDash, which pays around $19 per hour and requires about 53 hours to hit the same mark. If you have specialized skills like graphic design, writing, or programming, you can reach your savings goals much faster.

| Side Hustle | Median Hourly Rate | Hours to Earn $1,000 |

|---|---|---|

| Freelancing (Upwork) | $39 | 26 |

| Pet Sitter (Rover) | $22 | 46 |

| Virtual Assistant | $22 | 46 |

| Rideshare Driver (Uber) | $21 | 48 |

| Food Delivery (DoorDash) | $19 | 53 |

If specialized skills aren't your thing, service-oriented gigs like pet sitting or virtual assistant work - both averaging $22 per hour - are solid alternatives. You could also sell unused items on platforms like Facebook Marketplace or Poshmark for quick cash.

Ease of Implementation

Starting a side hustle has never been easier. Apps like Uber, DoorDash, and Instacart let you dive in quickly, offering flexible schedules that fit around your full-time job. These platforms are perfect for evening or weekend work without requiring long-term commitments.

To make sure your side hustle earnings go straight to your emergency fund, open a separate checking account and set up automatic transfers to a high-yield savings account. As Jason Fannon from Cornerstone Financial Services advises:

"Automation lets the money move before you can talk yourself out of it".

This approach not only builds your savings faster but also helps you avoid the temptation to spend your extra income.

Potential for Long-Term Financial Habits

Side work can do more than just pad your emergency fund - it can change how you approach your finances. For example, virtual assistants earn an average of $26 per hour and can potentially scale their income into six figures with the right connections. What starts as a short-term gig could grow into a steady second income.

Keep in mind, if you earn more than $400 from self-employment, you'll need to file an annual tax return and pay quarterly estimated taxes. The self-employment tax rate is 15.3%, covering Social Security and Medicare. To stay on top of this, consider setting aside 25% to 35% of your side earnings in a dedicated tax account.

Relevance to U.S. Financial Tools and Systems

Managing side hustle income is straightforward with U.S. banking options. Many banks offer tools like "savings vaults" or "buckets" within high-yield accounts, making it easy to separate your emergency fund from other savings goals. High-yield accounts also help your money grow faster than traditional savings accounts.

As of 2024, some employers are introducing workplace emergency savings accounts (ESAs), contributing between $100 and $1,000 per employee annually. If your employer offers this benefit, it’s worth exploring alongside your side hustle efforts to maximize your financial safety net.

5. Use a Separate High-Yield Savings Account

Stashing your emergency fund in a high-yield savings account (HYSA) can significantly speed up your savings growth. As of February 2, 2026, the best HYSAs offer annual percentage yields (APYs) between 3.30% and 4.35%, which is about seven times higher than the national average of 0.61%. To put this into perspective, a $10,000 balance in an account with a 4.5% APY could earn you approximately $450 in a year, compared to just a few dollars in a standard savings account.

Effectiveness in Accelerating Savings Growth

The higher interest rates offered by HYSAs let your money grow faster without requiring extra effort. Many online-only banks can provide these competitive rates because they save on costs associated with physical branches. Plus, your deposits are protected by FDIC or NCUA insurance, ensuring your funds are safe while earning more.

Ease of Implementation

Opening an HYSA is a simple process. Many top-rated accounts, such as those from LendingClub, EverBank, and Capital One, can be set up online in just a few minutes. These institutions typically charge no monthly fees and often have no minimum balance requirements. Once your account is ready, you can automate transfers from your checking account, making it easier to contribute regularly. Most transfers are processed within 1–2 business days, keeping the process smooth and efficient while helping you stay on track with your savings plan.

Building Long-Term Financial Habits

Separating your emergency fund into a dedicated account creates a mental barrier that discourages unnecessary spending. This separation helps you stick to your financial goals and maintain discipline over time. Many modern banks also provide digital tools that enhance your savings strategy, such as automatic goal tracking or notifications to keep you motivated.

Leveraging U.S. Financial Tools

Banks in the U.S. now offer features like digital "vaults" or goal-setting tools within their HYSAs, making it easier to track progress toward building a 3- to 6-month expense buffer. Some accounts, such as those from Capital One and Synchrony, even offer perks like ATM access or reimbursement of fees, ensuring you can quickly access cash in emergencies. When choosing an account, look for options with fast electronic transfers and user-friendly mobile apps for seamless money management.

| Institution | APY (Feb 2026) | Min. to Open | Monthly Fee |

|---|---|---|---|

| Newtek Bank | 4.35% | $0 | $0 |

| Openbank | 4.20% | $500 | $0 |

| LendingClub | 4.00% | $0 | $0 |

| Bread Savings | 4.00% | $100 | $0 |

| Capital One 360 | 3.30% | $0 | $0 |

Conclusion

Rebuilding your emergency fund takes steady effort and smart financial habits. By applying these five strategies - automating transfers, using expense-tracking tools like Monefy, allocating windfalls, earning extra income, and keeping a separate high-yield savings account - you can create a savings system that stands strong over time.

Think of your savings as a must-pay monthly expense. While financial experts suggest setting aside 5% of your monthly salary for emergencies, even starting small - like $10 to $50 a month - can lay the groundwork for a reliable safety net.

"Saving money is a marathon, not a sprint. It can pay to be intentional and take a long view."

- Navy Federal Credit Union

Breaking the process into smaller, manageable goals can make it feel less intimidating. Instead of aiming for 3 to 6 months of expenses right away, focus on initial milestones: $500, then $1,000, and eventually one month of living costs. These smaller victories build momentum and keep you motivated. As financial coach Marc Russell puts it, "your emergency fund is less about that broken water heater than about peace of mind." That peace of mind is knowing you won’t have to rely on high-interest credit cards or sacrifice long-term savings when the unexpected happens.

When you tap into your fund, replenishing it should become your top priority. Through automation, mindful spending, and consistent contributions, you can rebuild your financial cushion, protect your long-term goals, and reduce stress over life’s uncertainties.

FAQs

How does automating my savings make it easier to rebuild an emergency fund?

Automating your savings makes rebuilding your emergency fund much easier by ensuring regular contributions happen automatically. This steady approach keeps you on track and helps you reach your savings goal more quickly.

With automatic transfers, a portion of your paycheck goes straight into your savings account the moment you’re paid. This "set it and forget it" method reduces the urge to spend that money elsewhere, keeping your financial goals front and center.

Why is a high-yield savings account a good option for my emergency fund?

A high-yield savings account is an excellent option for building an emergency fund. Why? It offers higher interest rates than standard savings accounts, allowing your money to grow more effectively over time.

At the same time, it keeps your funds secure and readily available, ensuring you can access them quickly when unexpected expenses arise. This balance of growth, safety, and accessibility makes it a smart choice for safeguarding your financial cushion.

What’s the best way to track and cut back on unnecessary spending?

To keep unnecessary spending in check, start by drafting a clear budget that breaks down your expenses into categories. This makes it easier to spot areas where you’re overspending - like frequent takeout meals or forgotten subscriptions - and trim those costs to free up extra cash. Another smart move? Automate your savings. Set up automatic transfers on payday to consistently grow your emergency fund without the temptation to spend first.

It’s also important to regularly review your spending habits and make adjustments. Focus on covering essentials while scaling back on non-essential purchases. If you’re looking to boost your savings even more, consider selling items you no longer use or picking up a side hustle. Tools like Monefy can make this process easier by offering real-time expense tracking and insights, helping you stay on top of your finances and rebuild your emergency fund efficiently.